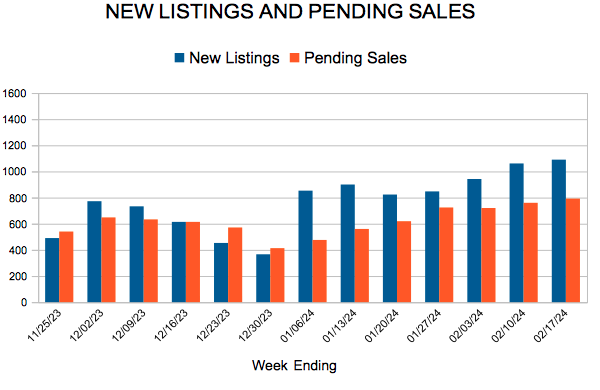

New Listings and Pending Sales

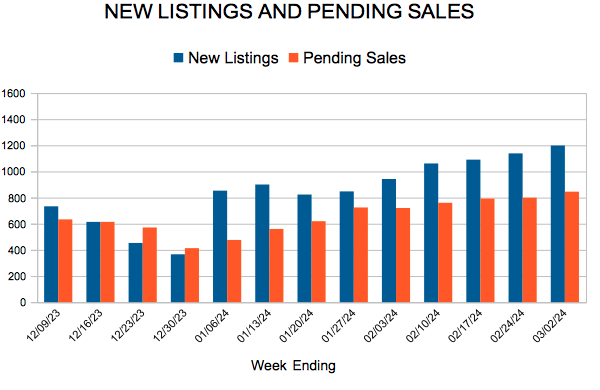

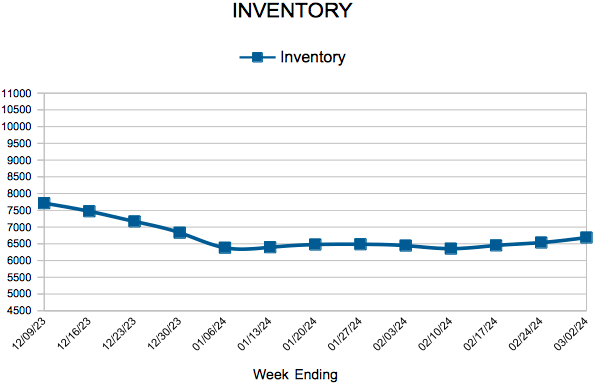

For Week Ending March 2, 2024

For Week Ending March 2, 2024

The limited supply of existing-home inventory nationwide continues to benefit the new-home market, with applications for new home purchases up 38% month-over-month and 19.1% year-over-year in January, according to the Mortgage Bankers Association Builder Application Survey. The latest reading marks the 12th consecutive annual increase and is the strongest non-seasonally adjusted reading for the month in the survey’s history.

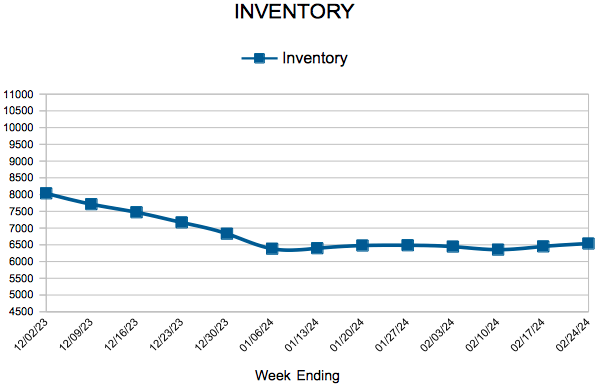

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING MARCH 2:

FOR THE MONTH OF JANUARY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

March 7, 2024

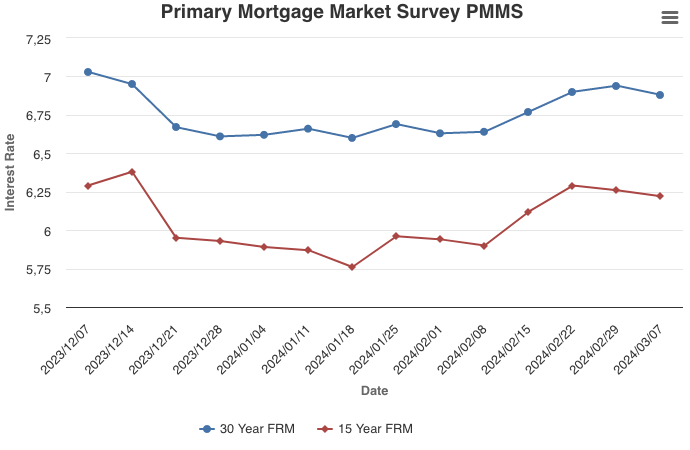

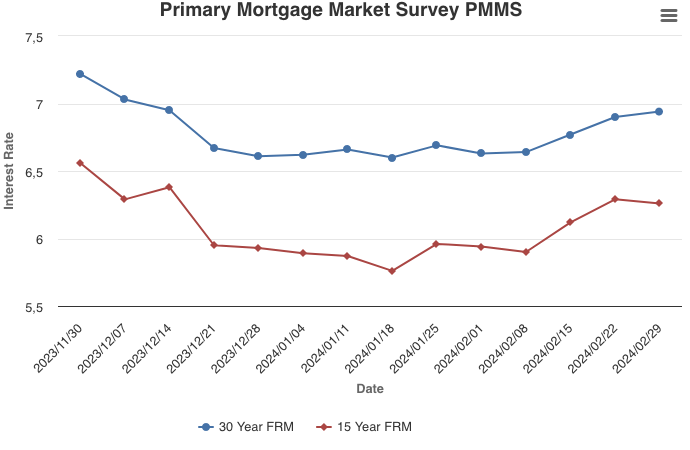

Evidence that purchase demand remains sensitive to interest rate changes was on display this week, as applications rose for the first time in six weeks in response to lower rates. Mortgage rates continue to be one of the biggest hurdles for potential homebuyers looking to enter the market. It’s important to remember that rates can vary widely between mortgage lenders so shopping around is essential.

Information provided by Freddie Mac.

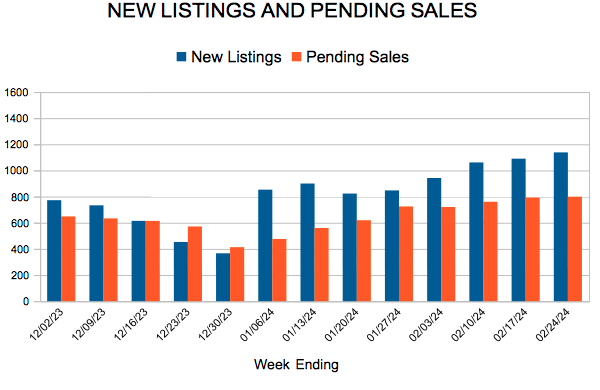

For Week Ending February 24, 2024

For Week Ending February 24, 2024

U.S. housing starts fell 14.8% month-over-month in January to a seasonally adjusted annual rate of 1,331,000 units, according to data from the U.S. Census Bureau. Single-family starts dropped 4.7% from the previous month, while multi-family starts declined 35.8%. Although construction was down for the month, builder sentiment continues to improve, rising to the highest level since August 2023, according to the National Association of Home Builders (NAHB) / Wells Fargo Housing Market Index (HMI).

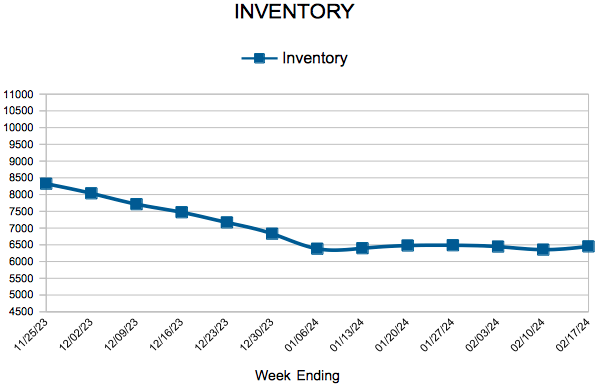

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING FEBRUARY 24:

FOR THE MONTH OF JANUARY:

All comparisons are to 2023

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

February 29, 2024

Mortgage rates continued their ascent this week, reaching a two-month high and flirting with seven percent yet again. The recent boomerang in rates has dampened already tentative homebuyer momentum approaching the spring, a historically busy season for homebuying. While sales of newly built homes are trending in a positive direction, higher rates and elevated prices continue to pose affordability challenges that may leave potential homebuyers on the sidelines.

Information provided by Freddie Mac.

Licensed In Minnesota

All information deemed reliable but not guaranteed and should be independently verified.