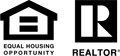

December 14, 2023

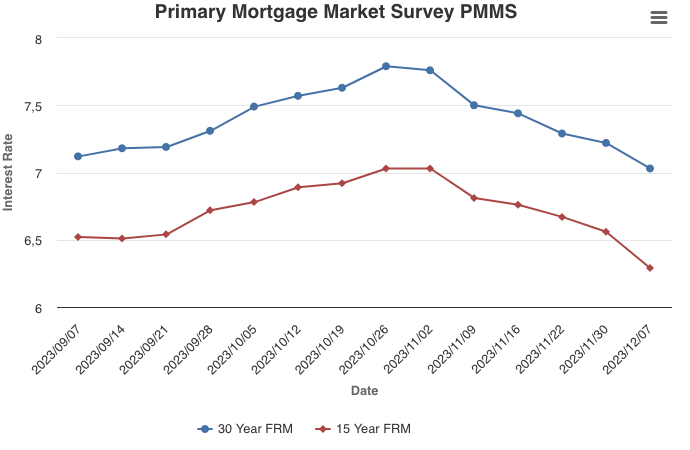

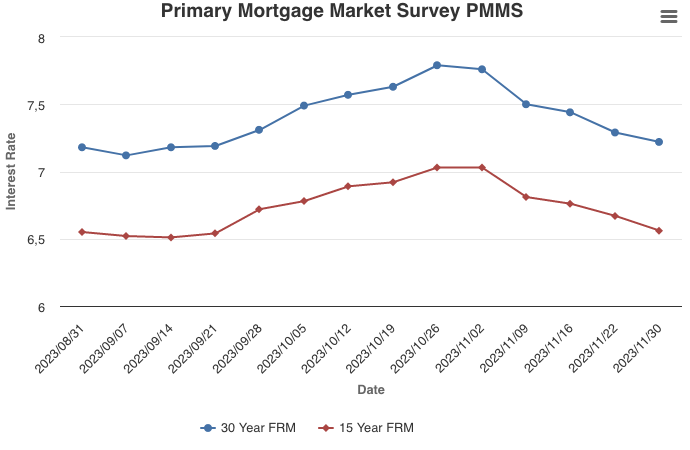

Potential homebuyers received welcome news this week as mortgage rates dropped below seven percent for the first time since August. Given inflation continues to decelerate and the Federal Reserve Board’s current expectations that they will lower the federal funds target rate next year, there will likely be a gradual thawing of the housing market in the new year.

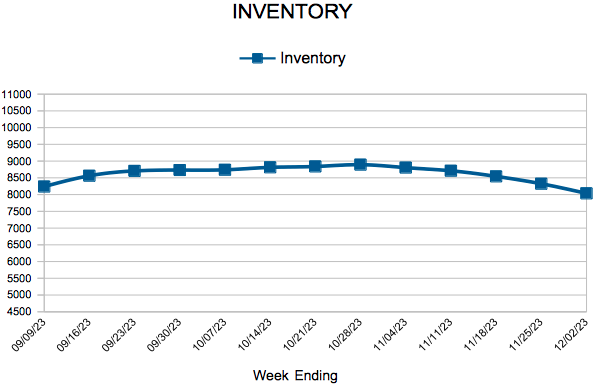

Information provided by Freddie Mac.

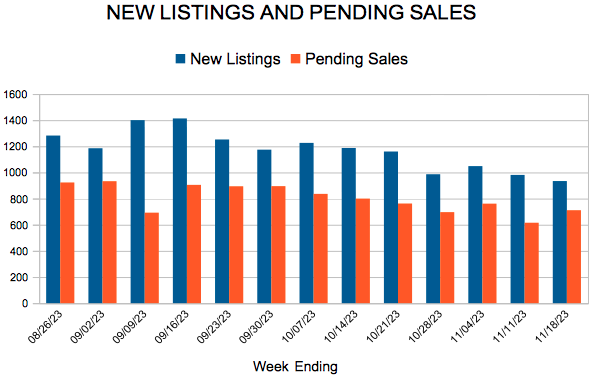

For Week Ending December 2, 2023

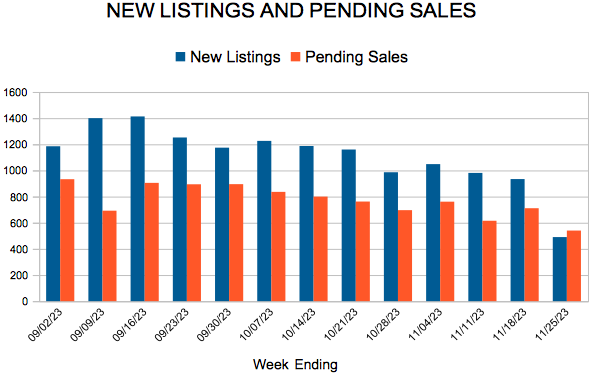

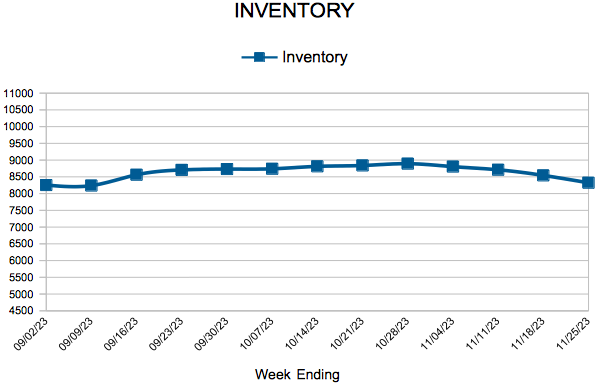

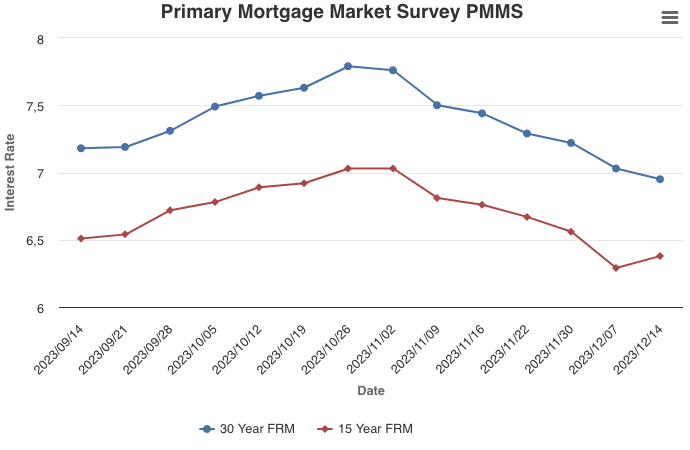

For Week Ending December 2, 2023