For Week Ending December 17, 2022

For Week Ending December 17, 2022

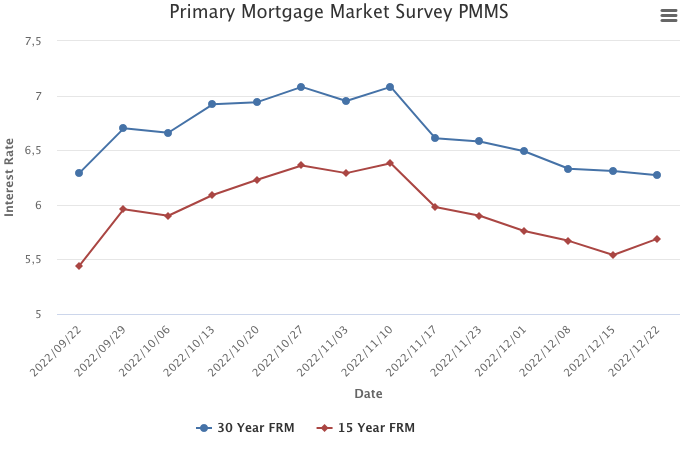

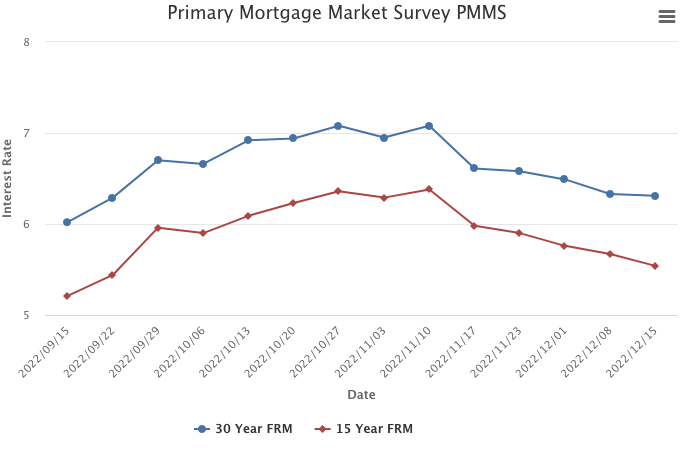

Mortgage rates continued their downward trend of recent weeks, as the 30-year fixed-rate mortgage averaged 6.31% the week ending 12/15, according to Freddie Mac. Mortgage rates have fallen for the past 5 weeks, declining by more than three-quarters of a percent in that time, and are at their lowest level since September. The drop in rates has resulted in an uptick in mortgage refinance demand, which increased 6% from the previous week, according to the Mortgage Bankers Association.

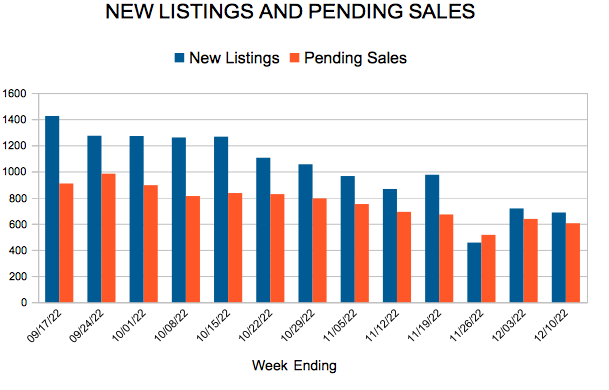

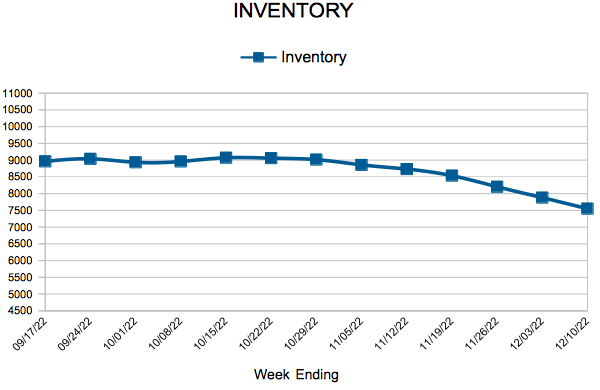

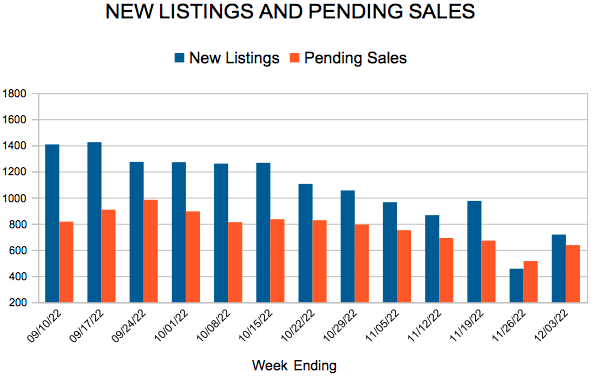

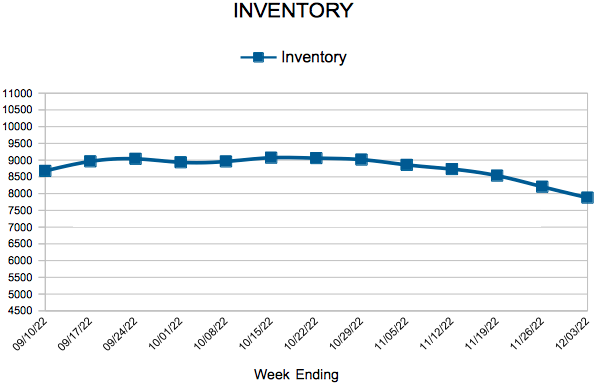

IN THE TWIN CITIES REGION, FOR THE WEEK ENDING DECEMBER 17:

- New Listings decreased 11.1% to 531

- Pending Sales decreased 23.2% to 633

- Inventory increased 17.1% to 7,258

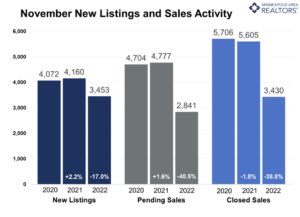

FOR THE MONTH OF NOVEMBER:

- Median Sales Price increased 4.1% to $354,000

- Days on Market increased 33.3% to 40

- Percent of Original List Price Received decreased 2.6% to 97.2%

- Months Supply of Homes For Sale increased 50.0% to 1.8

All comparisons are to 2021

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.